WMAMR

~

16 October 2024

~

开源项目

算法介绍

Weighted Moving Average Passive Aggressive Algorithm for Online Portfolio Selection (WMAMR):WMAMR是一种被动积极算法,用于在线投资组合选择,基于引入移动平均损失函数来实现多周期均值回归原理。该策略有效利用均值回归特性,提升了在线投资组合选择的表现。

模型信息

模型更新日期和预测日期:

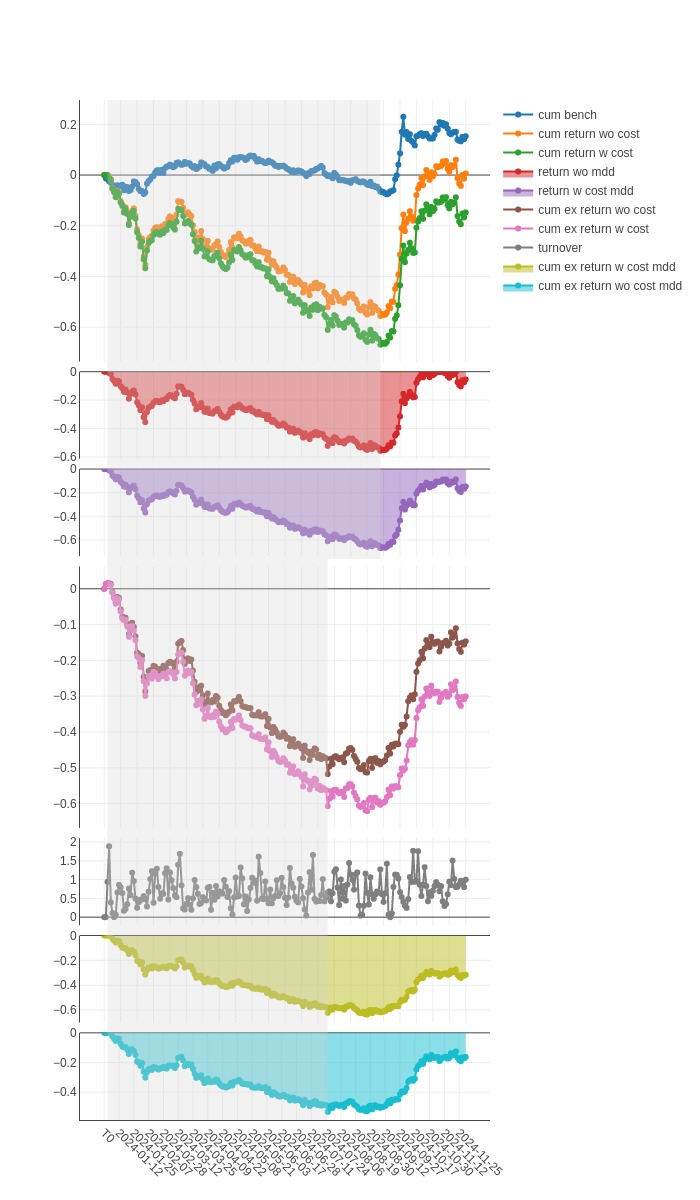

回测结果报告

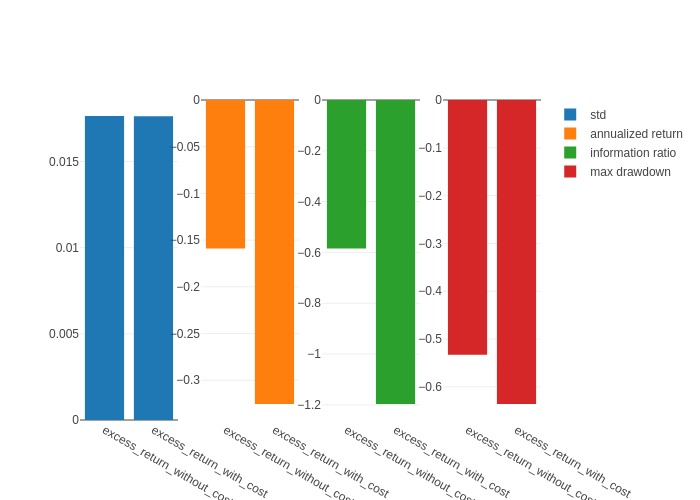

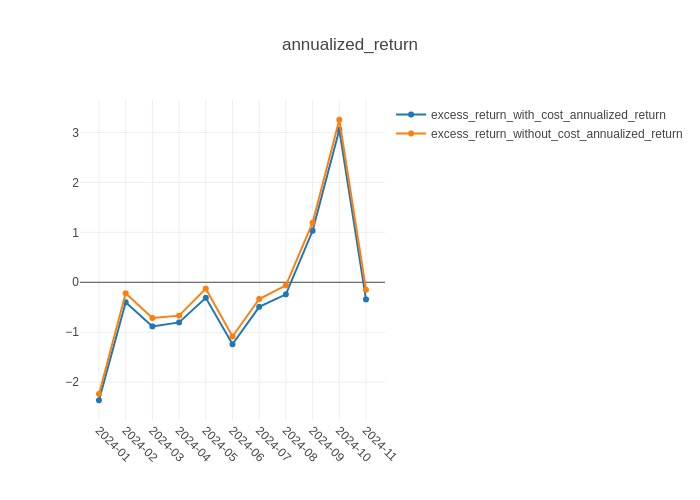

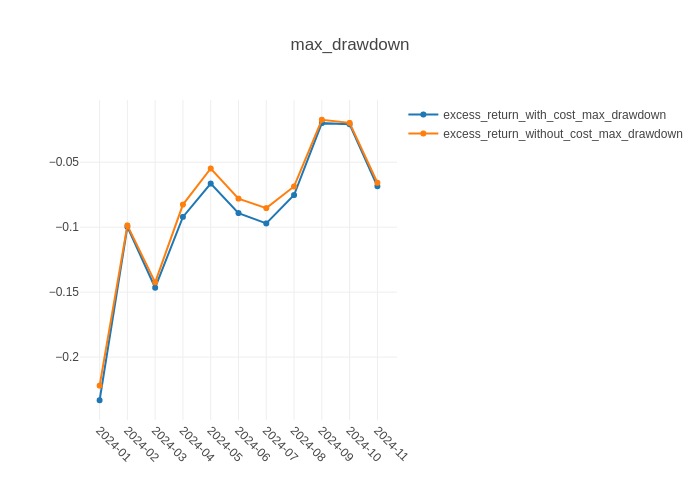

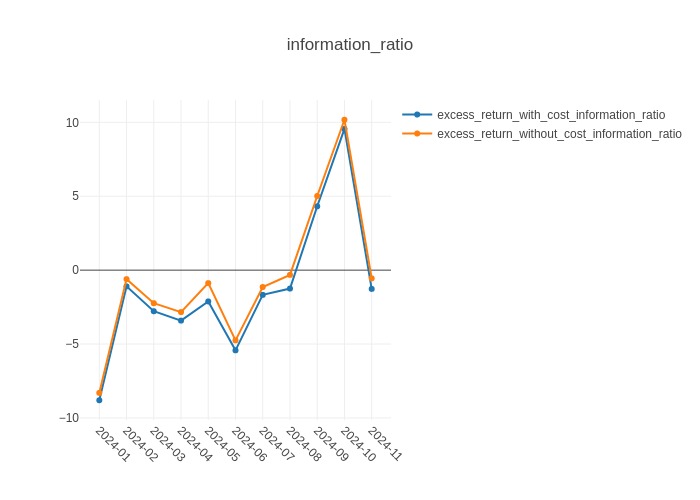

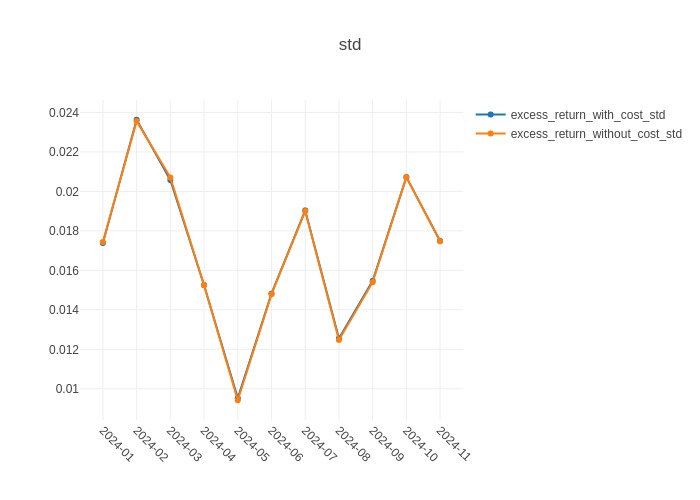

风险分析报告

参考文献

- Gao L, Zhang W. Weighted Moving Average Passive Aggressive Algorithm for Online Portfolio Selection[C]//Proceedings of the 2013 5th International Conference on Intelligent Human-Machine Systems and Cybernetics-Volume 01. 2013: 327-330.

Except where otherwise noted, this blog's content is licensed under a

Creative Commons Attribution 4.0 International License.

Except where otherwise noted, this blog's content is licensed under a

Creative Commons Attribution 4.0 International License.